Rethinking Employee Loans: From Relief to Resilience

Last Monday, I guested on the show ASPN (Ano Sa Palagay N’yo?) to discuss Good Debt vs. Bad Debt. You can watch that episode here.

I’ve discussed this topic a couple of times in my column like this one – Good Debt vs. Bad Debt. Debt has been with us for thousands of years. As discussed in FQ Book 1, debt originated as early as 3500 B.C., long before the advent of coinage or money in 600 B.C. In the same chapter, I also discuss the litmus test to distinguish good debt from bad debt.

For today, I wish to discuss another angle—how well-meaning loan assistance given by companies to their employees may sometimes not truly improve their financial condition. The intention is noble: We want to help our employees in times of emergency. We would rather extend the loan to protect them from predatory lenders.

But here is the quandary: While emergency loans are a “hero move” in the short term, they can unintentionally become a financial trap in the long run.

Let’s take a look at studies to see the potential hazards of good intentions versus behavioral realities.

1. The Moral Hazard (Why we stop building muscles)

Behavioral economics identifies a concept called Moral Hazard. When a safety net is too easy to access, we subconsciously stop taking preventive measures. If I know my company will always lend me money in times of emergencies, I am less likely to do the hard work of “paying myself first” to build my own Emergency Fund. We may stop building our saving muscles because the company provides a crutch.

2. The Pain of Paying is Anaesthetized

A study by Drazen Prelec and George Loewenstein on “tight coupling” explains that we feel actual psychological pain when we part with cash. However, employer loans are often paid through salary deduction. This “decouples” the consumption from the payment. You don’t feel the payment that much because it’s gone before it even hits your bank account. This makes it easier to borrow again and again without feeling the true weight of the debt.

3. The Debt-Stress Loop (Cognitive Scarcity)

Researchers Sendhil Mullainathan and Eldar Shafir (authors of Scarcity) found that financial stress creates a “bandwidth tax.” It lowers your effective IQ. When an employees’ take-home pay is eroded by loan amortizations, they live in a state of “scarcity,” making them more prone to impulsive decisions and less productive at work.

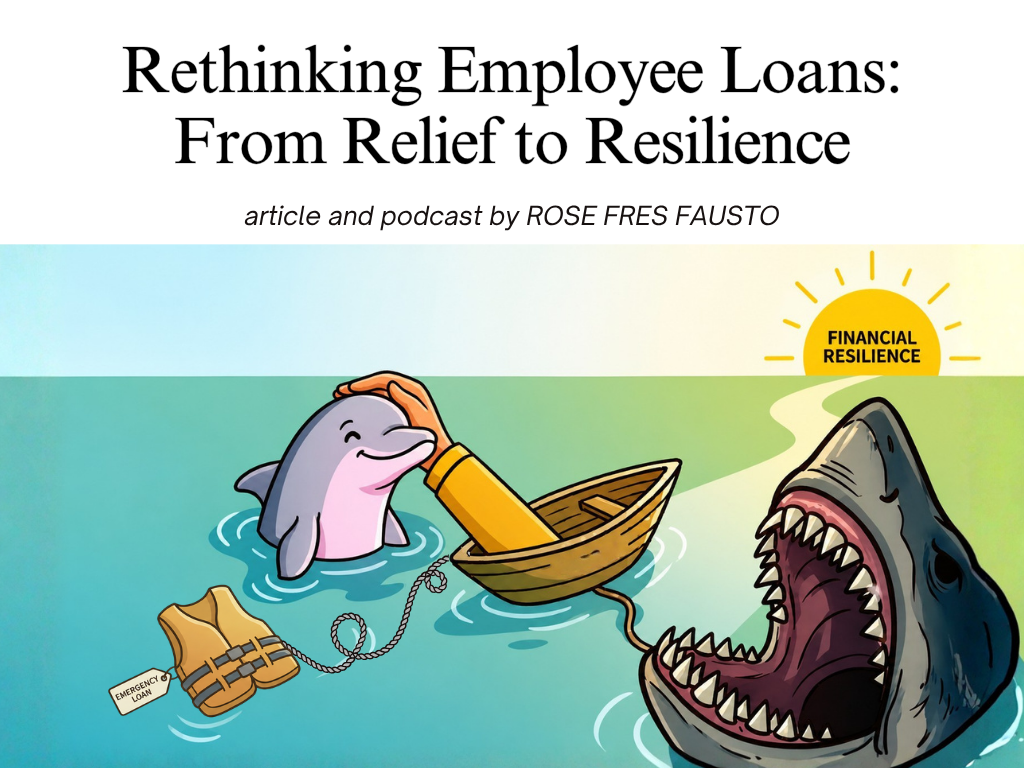

If we call predatory lenders as “loan sharks,” what can we call good-intentioned loans to employees—loan dolphins? They are friendlier and cheaper but they can still keep you underwater. When your salary is perpetually deducted, you may become a slave to the company—not because you love your job, but because you can’t afford to leave with an outstanding balance. This isn’t loyalty; it’s financial bondage.

So, what should employers do? We see some holding financial literacy initiatives. Unfortunately, as discussed in FQ Book 2, financial education alone does not work. Employers should provide the right salary disbursement structure, as discussed in FQ Book 3.

If you are an employer who truly wants to help, I’m not saying you should stop giving emergency loans to your employees in need. But study the actual effect of your well-intentioned loans. Then come up with the right structure that will make it easy for them to do what is right for the long term.

1. Build an Automatic Emergency Fund System

Instead of just offering a loan, help employees set up an automated savings program. A portion of their salary should be automatically deposited into a liquid emergency fund before they can spend it.

2. Matching Incentives: Instead of subsidizing interest on a loan, use that money to match an employee’s savings. If they save ₱500, the company adds its matching amount. This rewards the behavior we want to see (saving) rather than the behavior we want to avoid (borrowing for consumption).

3. Just-in-Time Friction: Add “healthy friction” to the loan process. Before a loan is approved, require a “budget stress test” that shows the employee exactly how his take-home pay will look for the next 12 months. This will help him visualize what’s in store for him.

True compassion isn’t just lending someone a life jacket every time they fall into the water; it’s helping them build a boat so they never fall in the first place.

Let’s help our Filipino workforce move away from Employer-Dependence and toward true Financial Resilience. Because at the end of the day, the best emergency fund is the one you own, not the one you owe.

ANNOUNCEMENT

- Does your money mindset work for you or against you? It’s time to move away from financial dependence and build your own saving muscles. Assess your financial quotient with our quick and insightful FQ Test. Know your score, learn your strengths, and take control of your financial future today.

- Want to master your money and avoid the hidden debt trap? Discover the history of debt, the limits of basic financial education, and how to set up the right savings structures. Complete your financial library and grab your copies of the FQ Books today! Shop FQ Books 1, 2, & 3 here.

This article is also published in Philstar.com