The “Someday” Trap

Can you believe we are already approaching the middle of 2026?

Take a moment to look back at the version of yourself when we started the year. Remember the fire, the resolutions, the goal-setting, the optimism and enthusiasm of the Fresh Start Effect? You likely had goals such as start healthy eating, regular exercise, sleeping on time, working well, reconciling with an estranged loved one, writing that book, starting your regular saving and investing, and other wonderful things that will make you a better version of yourself this year.

How’s your progress?

If you haven’t started yet, you might look at the calendar, realize it’s already May, and say, “I’ll just wait for the second half of the year to start fresh.” Or worse, “Next year na lang.” If so, you are now falling into the dangerous Someday Trap!

Let’s discuss this in a context that’s more quantifiable: Your finances. If you lose your enthusiasm to start now because you missed the “New Year Bus,” this Someday Trap can turn out to be the most expensive mental loop in your financial life.

We often wait because we think we need more information, more money, or more stability to start. But in Behavioral Economics, we know the real culprit is Inertia. (Remember M I LA, the biggest barriers to retirement saving?

We stay still because starting requires a force of activation. And while standing still feels safe, when it comes to investing, it is actually a dangerous move (or should I say, non-move?). Let’s take a look at two characters and their retirement nest eggs to see how they are affected by the power of inertia.

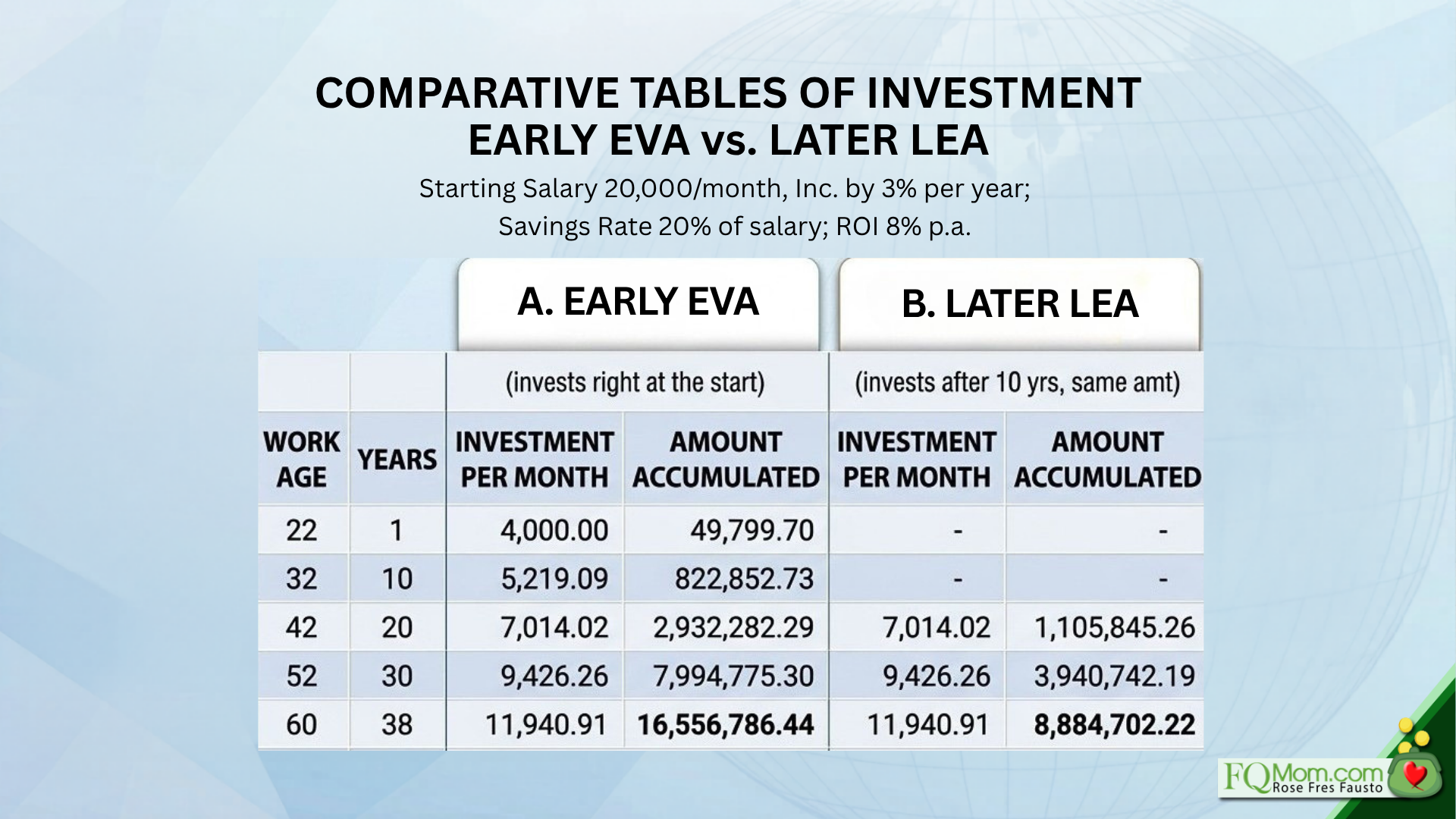

Meet Early Eva and Later Lea

Early Eva and Later Lea started working at the same time, earned the same starting salary of Php 20,000 per month. While Early Eva started her saving and investing 20% of her salary right away, Later Lea decided to YOLO her way for 10 years. She figured, “I’m still young, I can start saving and investing after 10 years. I’ll have enough time to catch up.” Was she right? Let’s take a look at what her Someday Trap did to her retirement nest egg.

The table above shows that Later Lea was dead wrong. Succumbing to the Someday Trap and wasting the power of compounding in her first 10 years cost her a fortune. She ends up with only Php 8.88 million versus Early Eva’s Php 16.56 million. Even if she just squandered 10 years out of the 38 years, she lost almost half of what she could have accumulated for her retirement nest egg.

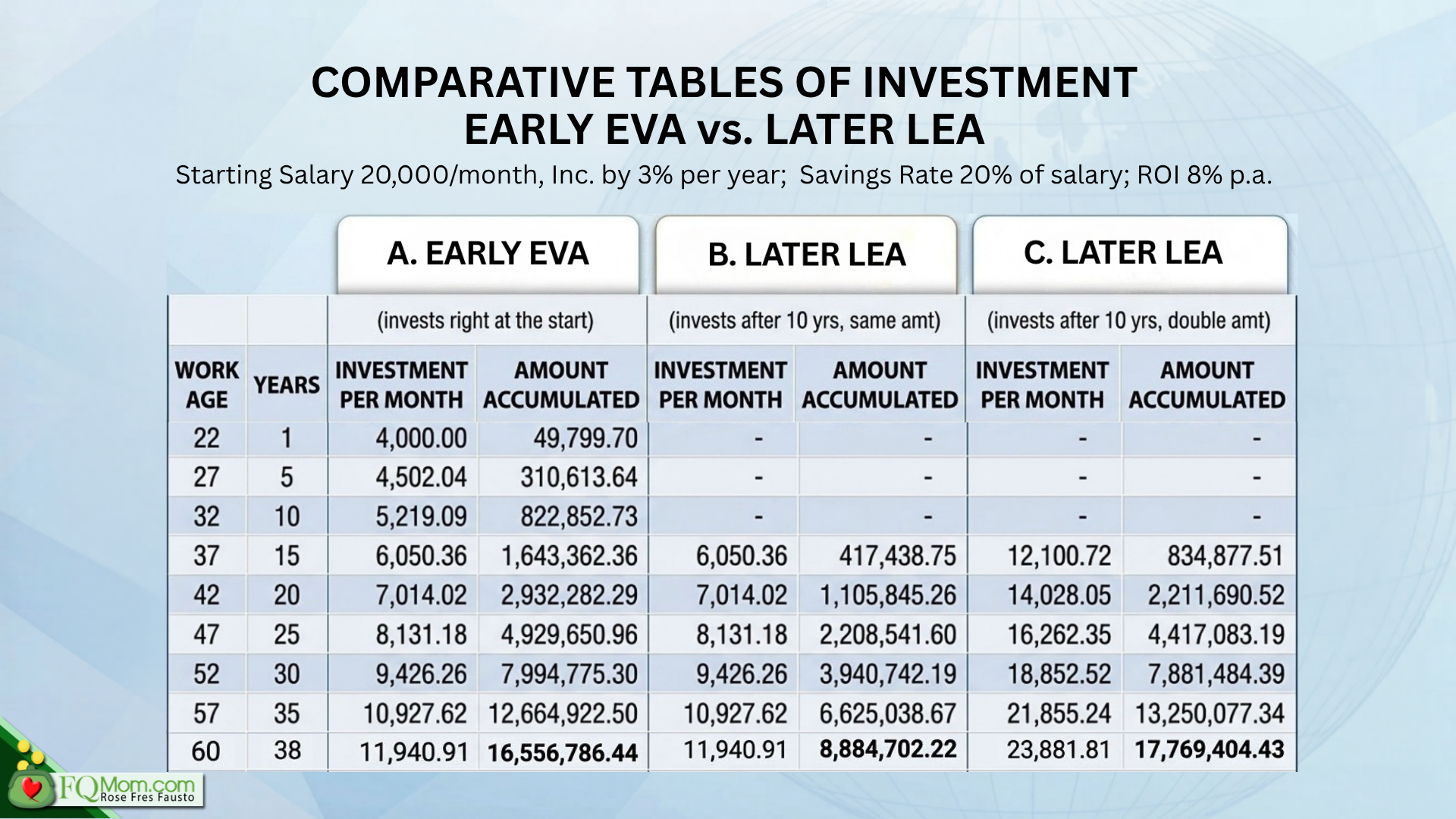

Supposing Later Lea decides to double her saving and investing rate to 40% so she can make up for lost time and hopefully surpass Early Eva’s steady 20%. What do you think will happen?

Unfortunately, even with double savings rate, Later Lea will have a hard time catching up with Early Eva—not after 20 years or 30 years, but only when they finally reach the retirement age of 60. And here’s the thing: Do you think someone who spent 100% of her income for the first 10 years can suddenly have the discipline to live on 60%? Do you think someone can suddenly go from 0% savings rate to 40%? Between the two, who is more likely to increase her savings rate over time?

This is the power of compounding and the importance of time—your greatest ally in investing. Your Emotional Emong side will always have a reason to procrastinate, but I hope your Makatwirang Mak side now sees how the Someday Trap is indeed a wealth killer!

If you missed the “first job bus” or the “New Year bus,” it is still better to do something now than just throw in the towel. As a Chinese proverb says:

“The best time to plant a tree was 20 years ago. The second best time is now!”

Break the Inertia

If you are ready to break the inertia and finally activate your wealth building system, I want to help you do it—not “someday,” but this weekend.

This coming Saturday, May 16, at 2 PM, Bianca Gonzalez and I are holding an intimate High FQ Design Workshop at the Tektite Tower in Pasig City. This isn’t a lecture where you just take notes; it’s an Activation Day.

We are going to:

- Identify your unique money memory to stop the self-sabotage.

- Design an environment that makes saving and investing automatic.

- Actually open and activate your investment accounts right there and then.

We’ve kept the rate at a special subsidized amount of ₱1,000 to eliminate the “It’s too expensive” excuse that your Emotional Emong might use to keep you in the Someday Trap.

The choice is yours. You can finish 2026 exactly where you were financially at the end of 2025, or you can break the inertia this weekend. Let’s turn your May midpoint check-in into a turning point in your financial wellbeing.

If you choose the latter, click here to register and I’ll see you on Saturday.

This article is also published in Philstar.com