The Disposition Effect: Why we sell our winners and keep our losers

Have you ever experienced selling your winning stocks too soon but holding on to your losing stocks for too long? If you have, you are not alone as this is a common pitfall in investing. Understanding why this happens will help you improve your FQ.

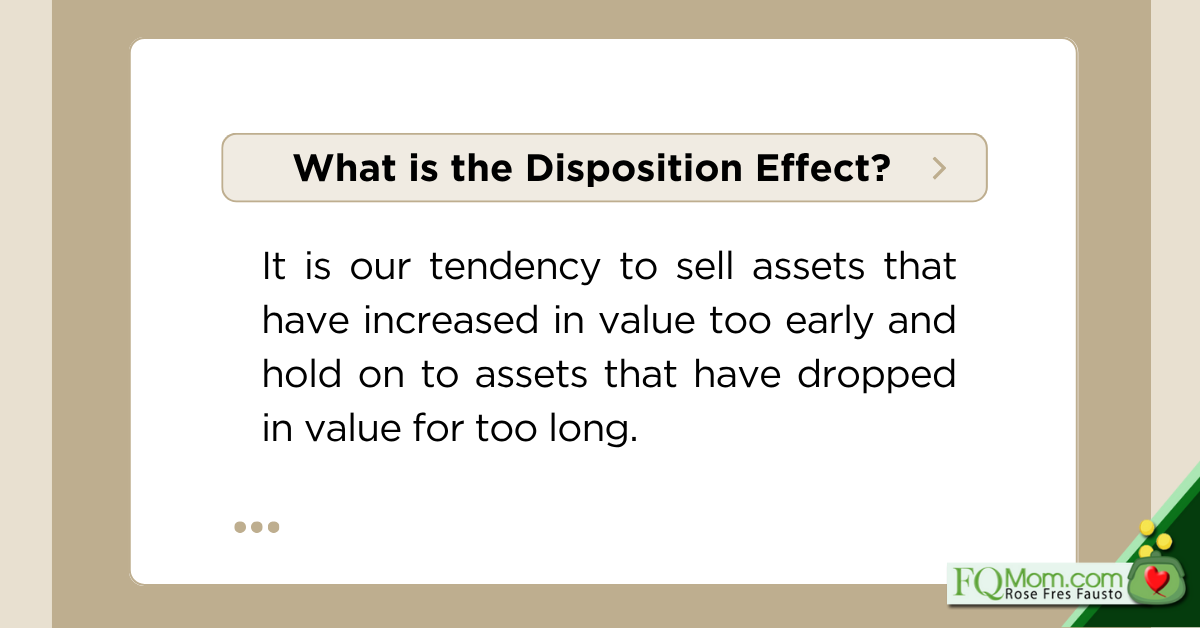

What is the Disposition Effect?

It is our tendency to sell assets that have increased in value too early and hold on to assets that have dropped in value for too long. We are quick to take a small win but hesitant to accept a loss, even when logic tells us we should do the opposite.

The term was first coined in 1985 by behavioral finance researchers Meir Statman and Hersh Shefrin in their paper The Disposition to Sell Winners Too Early and Ride Losers Too Long: Theory and Evidence. Their research challenged the classic financial theory that assumes investors always act rationally. They found compelling empirical evidence that people are driven by their emotion and psychological biases when making investment decisions.

An example:

Makatwirang Mak and Emotional Emong both bought Stock A and Stock B at Php100/share. After a week, Stock A is trading at Php120/share while Stock B is at Php 80/share. After evaluating the two stocks, Mak holds on to Stock A and sells Stock B, while Emong does the opposite. Most investors would act like Emong and say, “I’ll sell Stock A now and take the profit. I’ll hold on to Stock B and wait for it to recover, sayang naman!”

On the surface, Emong’s argument to sell the winner and hold on to the loser may sound reasonable but here’s the catch: the decision to sell or hold should be based on the stock’s future potential. Selling a strong stock too early means you might miss out on more growth while holding on to a weak stock may only increase your losses.

The anatomy of falling into the Disposition Effect

Here are some behavioral biases discussed in FQ Book 2 that explain why we tend to fall into the trap of the Disposition Effect.

- Loss Aversion – discussed in Chapter 6 as our tendency to feel the pain of a loss at least twice as much as that of a gain. Result: We avoid selling Stock B, the loser stock.

- Sunk Cost Fallacy – discussed in Chapter 8 as our tendency to throw good money after bad, continuing a behavior just because of previously invested resources and without due regard of what the current and future costs and benefits are. In the example, most Emongs would not only hold on to Stock B but also buy more, just like what happened in the Concorde Effect from 1954 to 2003! (Also discussed in Chapter 8)

- Mental Accounting – discussed in Chapter 14 as our tendency to treat money depending on where it comes from and where it is going forgetting that money is fungible. In the above example, it’s Emong’s tendency to treat each stock investment separately, instead of looking at his portfolio as a whole.

- Pride and Regret – selling a winning investment makes us feel smart while selling a losing one makes us feel like admitting we made a mistake, experiencing regret. The consequence is hanging on in the hope of redemption.

Conquering the Disposition Effect

How does a high FQ person design his investment environment to avoid this pitfall?

- Design a clear investment strategy. Define your goals, risk tolerance, and investment horizon with entry and exit points.

- Create rules in advance. Decide beforehand when you’ll sell. You can use percentage-based rules (e.g., Sell if stock falls by 20%) in order to take the emotion out of the decision making. Consider using automated investment platforms or setting up stop-loss orders.

- Diversify. A diversified portfolio helps cushion the blow of individual losing investments, making the pain less acute and reducing the urge to hold on desperately.

- Focus on the big picture. Review your portfolio as a whole on a periodic basis. Use this question as your guideline: What asset allocation will help me meet my goals?

- Reframe the loss. Instead of seeing a loss as a personal failure, view it as a smart move: I’m reallocating my money to something with better growth potential.

- Educate yourself continuously. Your behavioral biases also form part of who you are. That is why unlike in the FQ Score, where I want you all to get as high as 100%, it’s not the same for your Makatwirang Mak/Emotional Emong or ME Score. What’s important is you are aware of your biases so you can properly design your environment in order to make it easier for you to do the right thing.

- Automate the parts that you can. While investing if for everyone, stock picking and trading is not for everyone. That is why I always advise everyone to just invest in equity index funds for their longer-term investments, and to automate it via programs of your chosen financial platform.

Final Thoughts

As high FQ investors, we don’t just celebrate our gains, we also know when to cut our losses! By the way, Dr. Meir Statman, one of the two who coined the term Disposition Effect, was once here in the country to give a talk to the Fund Managers Association of the Philippines (FMAP). He is considered one of the fathers of Behavioral Finance. I had the privilege and pleasure of interviewing him then. Let me share with you my FQwentuhan with Dr. Statman where you will get other valuable behavioral insights.

ANNOUNCEMENTS:

- Take the FQ Test to know where you are in your FQ journey. click here.

2. Improve your FQ Score and those of your loved ones, get your copies of FQ Book 3 or the complete trilogy for the discounted bundle price. Click here.

This article is also published in Philstar.com