There is Romance in Asset Allocation!

Last Friday my husband and I did our usual Wedding Anniversary Day (or days) Off. It has been our tradition for the last 27 years! It all started when Manila Hotel (where we held our reception) gifted us with a free accommodation on our first wedding anniversary. So even if our honeymoon baby was only three months old then, we took a day off, just the two of us. Thanks to my mom, she was always our reliable guardian in times like this.

On our anniversary day, we still do the cheesy stuff. Marvin gives me a bouquet of flowers then we go off to a resort or a hotel we haven’t been to (or maybe one with free accommodation which we would occasionally receive as a gift). We’d watch bits and pieces of our wedding album and video (which was originally in Betamax) and reminisce about that eventful day, the 12th of August 1989. As the years went by, these pieces of memorabilia have been expanded to include our Tin (10th), China (20th) and Silver (25th) anniversaries. Yes we’ve said “I do” in ceremonies four times already. In fact, every single year we renew our vows privately during our anniversary.

What else do we do?

Marvin and I are admittedly romantic and we think this is one of the things that help keep our marriage alive. But on our anniversary, we also get down to business. We visit our Balance Sheet together and review our Asset Allocation! We’re weird that way, you know. 🙂

What is Asset Allocation? It is an investment strategy that attempts to balance risk versus reward by adjusting the percentages of the asset classes in your investment portfolio. Whether you are aware or not, you are implementing an asset allocation and this will play an important role in your wealth accumulation; consequently, the quality of your married life in your ripe old age.

Why is Asset Allocation important? Asset Allocation is the probably the most important investment strategy, even more important that stock picking, timing, etc. It’s because nobody can really predict the movements of the financial markets, the economy, both local and global, and this strategy helps you protect your portfolio from market ups and downs, by spreading your risk among the different asset classes.

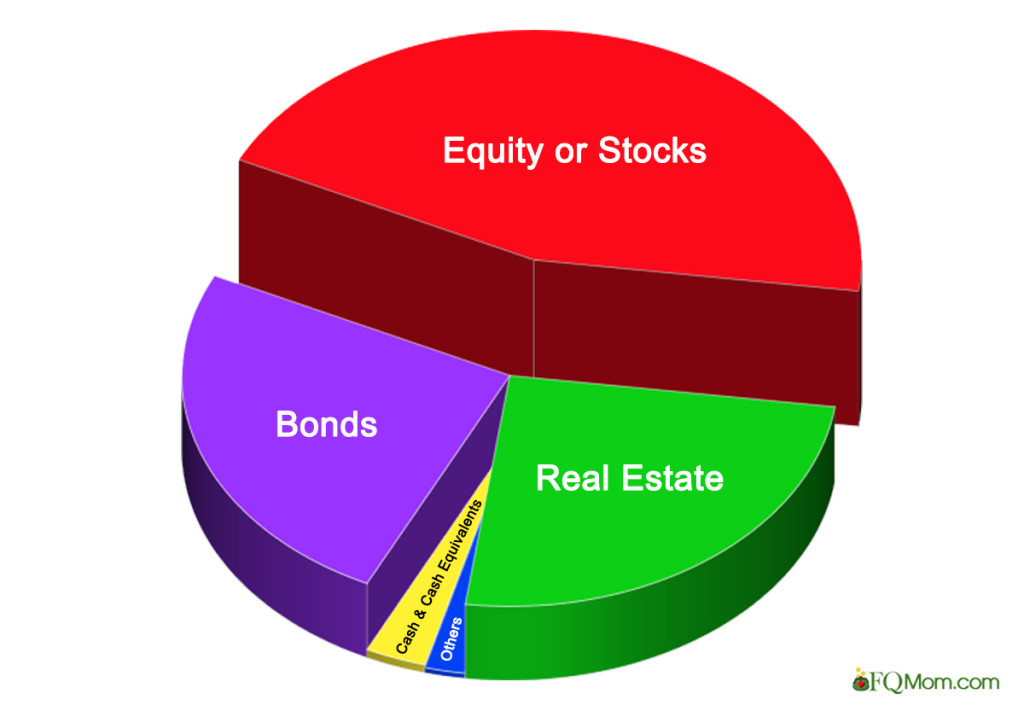

Asset Classes. A couple may (or should I say should?) invest in the following asset classes:

- Cash and other Cash Equivalents – cash on hand, savings and current accounts, time deposits, money market placements. These are highly liquid instruments with maturity of three months and below.

- Bonds – are debt instruments in which you, (the investors) lend money to the bond issuer, usually a corporation or the government. It has a defined tenure and an agreed-upon interest rate.

- Equity or Stocks – an investment that signifies ownership in a corporation, giving you a claim in the assets and earnings of a corporation.

- Real Estate – your house, if you own one, usually makes up a significant part of your portfolio. This may also include other real estate properties purchased for investment purposes either for rental income or asset appreciation for eventual sale.

- Others – these are your other properties of value such as paintings and other art pieces, jewelry, etc. For more savvy couples, they may also have gold, commodities, forex and other investment instruments.

*Note that you may invest either directly or through pooled funds (Mutual Funds or UITFs – Unit Investment Trust Funds) when buying stocks, bonds and money market instruments. Pooled Funds for real estate (REITs), gold and other commodities are not yet available in our country.

How to allocate. There are various prescribed allocations being recommended out there. Let me share what the three investment icons, Benjamin Graham, John Bogle and Warren Buffett have to say about asset allocation.

- Benjamin Graham’s 50:50 Stocks and Fixed Income.

The mentor of Warren Buffett and author of investing bible The Intelligent Investor said, “We have suggested as a fundamental guiding rule that the investor should never have less than 25% or more than 75% of his funds in common stocks, with a consequent inverse range of 75% to 25% in bonds. There is an implication here that the standard division should be an equal one, or 50-50, between the two major investment mediums.”

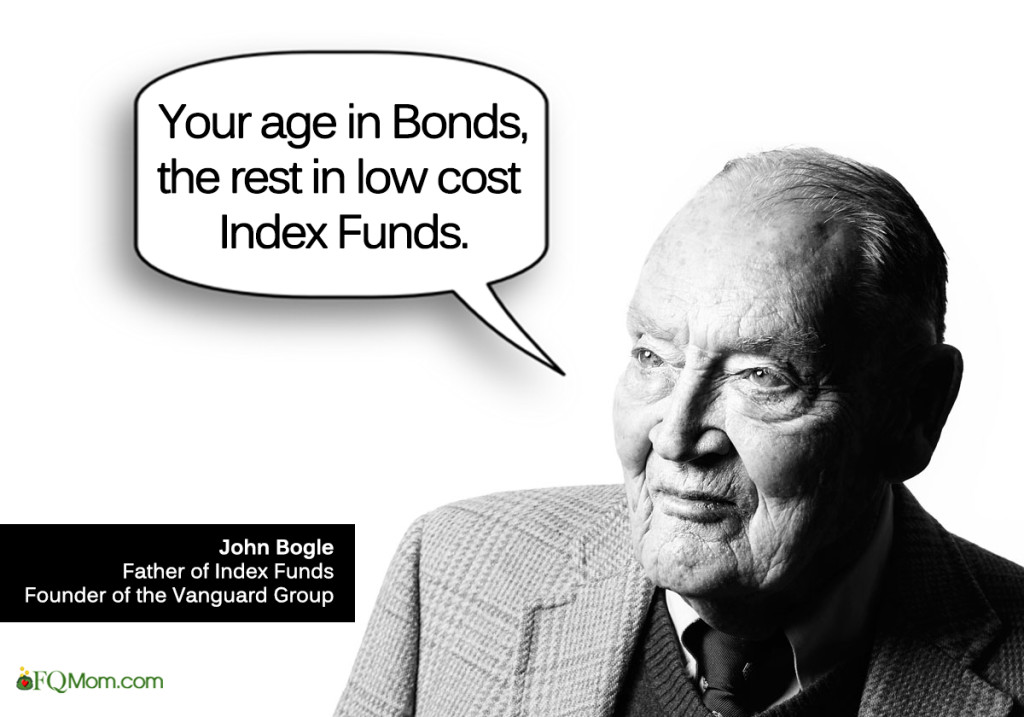

- John Bogle’s Your Age in Bonds.

The Father of Low Cost Index Funds and founder of Vanguard Group said in his book Common Sense on Mutual Funds, “I recommend as a crude starting point that an investor’s bond position should be equal to his age.” This is very similar to the 100 minus Age equals Stocks, which is now being adjusted to either 110 or 120 less age due to the longer life spans we are now experiencing.

- Warren Buffet’s 90:10 Low Cost Index Funds:ST Gov’t Bonds.

The world’s greatest investor said in his 2013 Letters to Berkshire Hathaway Shareholders that upon his passing the trustee of his wife’s inheritance was instructed to put 90% of her money into low-fee index funds and 10% into short-term government bonds.

Please take note that the above asset allocations are based on two basic asset classes only – fixed income bonds and stocks. These are rules of thumb from the investment icons and as in any rule of thumb, it provides us a quick and easy starting point. It works well for couples or individuals who are just starting a portfolio.

Instead of limiting yourself to any of the above formula or the others you will find in various sources, I suggest you come up with your own. Discuss it as a couple and bear in mind the important things to consider in your asset allocation.

Things to Consider in your Asset Allocation

- Goals. What are your goals as a married couple? As a family? Each goal has a corresponding price tag and timetable. What kind of retirement do you want to have? Try to match each goal with the best asset class.

- Age. How old are you? How much time do you have in fulfilling those goals?

- Risk appetite vs. Reward. What’s your risk appetite? Remember the risk return trade off? The higher the return, the higher the risk. The lower the risk, the lower the return. So figure out what the right mix is for you. It will also help if you include assessing what you’re good at. Some people who are good at spotting real estate deals may well include a good portion of this in their portfolio. This can also be true in the other asset classes like art pieces, etc.

All of the above will help you come up with the best asset allocation for your own needs. What is great about periodically checking your asset allocation is that you are able to update your financial journey in line with your life goals and dreams. Your goals and dreams change as you move from one life stage to another. So should your asset allocation. The regular assessment will remind you to re-balance. Rebalancing is quite difficult because it is counter-intuitive. It asks you to sell the asset class that’s doing well and buy the one that’s not doing so well. So this exercise of regular assessment will nudge you to do it.

There is romance in Asset Allocation.

Some think that money is the least romantic thing. Talking about it may bring about uneasiness, stress, etc. This is the reason why many couples do not talk about money deliberately. Unfortunately, not being deliberate about where you put your money is what brings about the loss of romance! I’m not kidding. Studies show that seven out of ten marital problems are about money.

So the next time you celebrate your wedding anniversary, you may want to include Asset Allocation in your lovey dovey agenda. Make it fun! 🙂 It’s an opportunity to share your big dreams and carry on your journey in unison.

I also invite single persons to include this on their birthday assessment. Whether you’ll get married or not, it is something that you should be deliberate about.

May you reach all your dreams through your sound asset allocation!

******************************

ANNOUNCEMENTS

- Do you want to know your FQ Score? Click link below to take the test.

- Join the FQ Meme Challenge

3. Watch out for my FQ talks in cooperation with Security Bank. Dates and venues to be announced.

3. Watch out for my FQ talks in cooperation with Security Bank. Dates and venues to be announced.

Rose Fres Fausto is a speaker and author of bestselling books Raising Pinoy Boys and The Retelling of The Richest Man in Babylon (English and Filipino versions). Click this link to read samples – Books of FQ Mom Rose Fres Fausto. She is a Behavioral Economist, Certified Gallup Strengths Coach and the grand prize winner of the first Sinag Financial Literacy Digital Journalism Awards. Follow her on Facebook and You Tube as FQ Mom, and Twitter & Instagram as theFQMom.

ATTRIBUTIONS: Photos from clker.com, forbes.com, gettyimages.co.uk, kids.nationalgeographic.com, kidscountry.com, usstockoption.com, wire.kapitall.com put together to deliver the message of the article.